Iberdrola Cloud Win Reveal Its Edge in Complex Digital Transformations?")

- Iberdrola recently announced that it partnered with DXC Technology to complete one of Spain’s largest and most complex IT modernization projects, migrating 180 terabytes of data and more than 30 million lines of code to Microsoft Azure’s cloud environment.

- This transformation not only enhances Iberdrola’s operational agility and supports AI integration, but also enables seamless compliance and model replication across various regions.

- To better understand DXC’s investment appeal, we’ll explore how this major cloud migration showcases its expertise in large-scale digital transformation.

Find companies with promising cash flow potential yet trading below their fair value.

DXC Technology Investment Narrative Recap

To be a DXC Technology shareholder right now, you need to believe that the company can convert its high-profile digital transformation wins into stable, sustainable revenue, despite ongoing organic declines and segment pressure. The Iberdrola cloud migration demonstrates DXC’s ability to deliver complex transformation at scale, but this news does not materially change the most urgent short-term risks, which remain centered on persistent revenue contraction in core areas and future deal conversion.

Among recent announcements, DXC’s collaboration with 7AI to launch an Agentic Security Operations Center closely aligns with its focus on next-generation digital and AI-enabled offerings. This supports the company’s stated catalyst of using advanced technology partnerships to lift average deal size and generate more recurring revenue, which could help offset headwinds in legacy segments if conversion rates stay strong.

However, despite these positive moves, it’s worth noting that ongoing declines in the Global Infrastructure Services segment mean investors should remain aware that…

Read the full narrative on DXC Technology (it’s free!)

DXC Technology’s outlook projects $12.1 billion in revenue and $208.6 million in earnings by 2028. This reflects a -1.7% annual revenue decline and a decrease of $170.4 million in earnings from the current $379.0 million.

Uncover how DXC Technology’s forecasts yield a $15.12 fair value, a 8% upside to its current price.

Exploring Other Perspectives

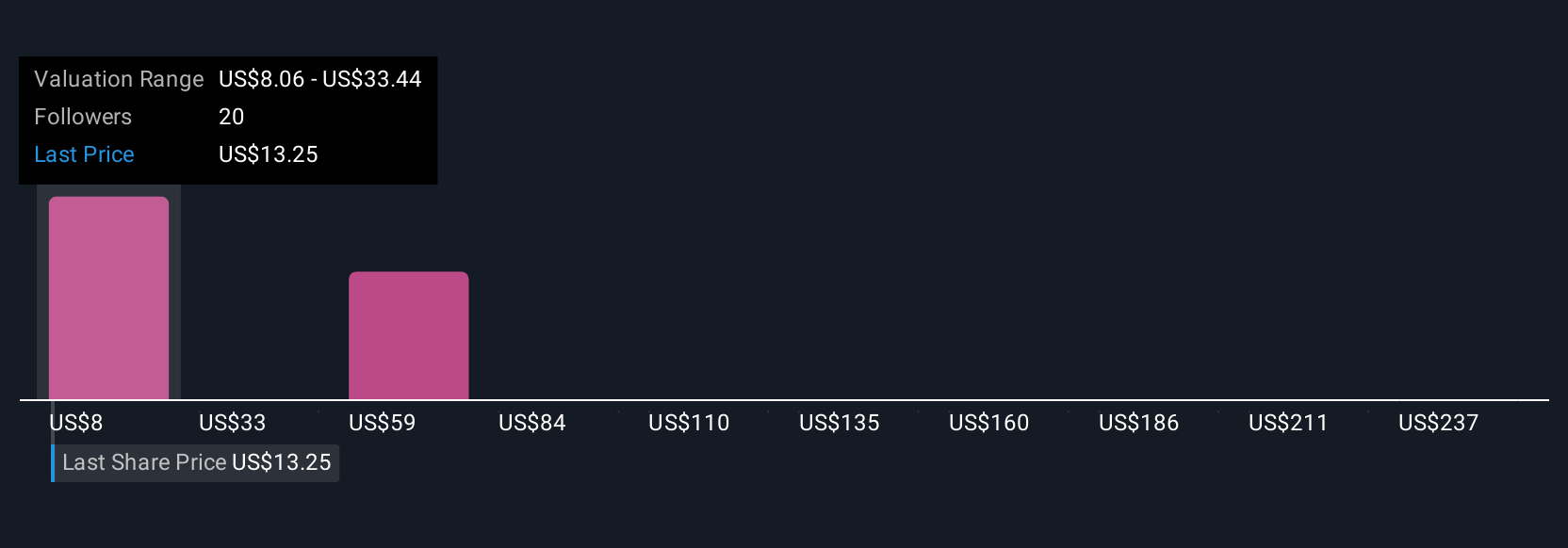

Simply Wall St Community members provided six unique fair value estimates for DXC ranging from US$8.06 to US$261.89. While these perspectives show broad disagreement on valuation, the company’s struggle to stabilize core revenue still weighs heavily on overall sentiment.

Explore 6 other fair value estimates on DXC Technology – why the stock might be worth 43% less than the current price!

Build Your Own DXC Technology Narrative

Disagree with existing narratives? Create your own in under 3 minutes – extraordinary investment returns rarely come from following the herd.

Curious About Other Options?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Try a Demo Portfolio for Free

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email [email protected]

link